It can be hard to fathom the impact of the pandemic on the data center supply chain. Demand generated by the overnight explosion in work-from-home and the accelerated digitization of our day-to-day lives has raised the stakes across the board.

An acute IC shortage has not helped matters, with reports of lead times stretching to 50 weeks as demand exceeds current fab capacity. Meanwhile, companies are grappling with runaway logistic costs and long waits at ports as manufacturers embrace ocean shipping as an alternative to the restricted capacity and sky-high costs of air freight.

The data center supply chain is riding the waves of a global storm, with consequences that will long outlive the current moment.

In our latest Storage Market Brief, we explore the state of the international market for data center hardware, from the global chip shortage to the outlook for HDD in an increasingly flash-first world.

International Tensions Drive Supply Chain Rethink

Although the end of COVID is seemingly near—among developed nations, at least—the coronavirus continues to leave its mark.

Governments are left to balance the health of their citizens against the health of the economy. New variants raise concern about when the pandemic’s end will truly arrive. Most tellingly perhaps, the pandemic has exposed—in some cases exacerbated— geopolitical differences as countries vie for resources, vaccines, and critical technology.

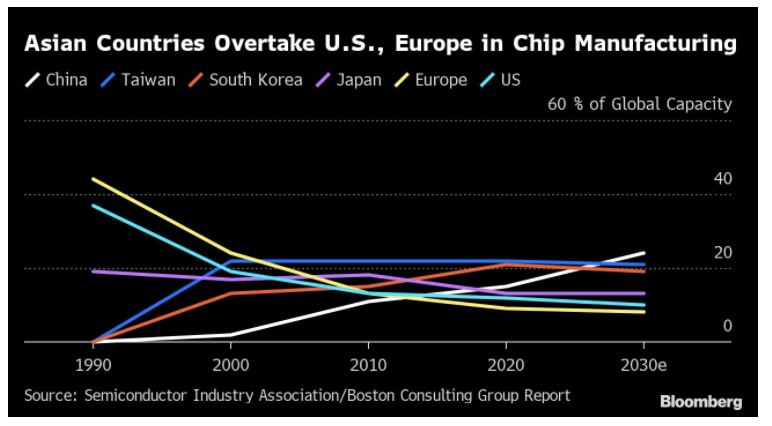

Take the well-documented rivalry between the United States and China. Long-standing tensions over domain knowledge and IP have revealed some of outsourcing’s limitations, with the U.S. banning shipments of critical technology to Chinese entities.

For its part, China has been upfront about its desire to achieve technological self-sufficiency and emerge as the global technology leader through its Made in China 2025 initiative.

Desperately Seeking Chips

Meanwhile, the struggles of the automobile industry—historically a source of pride for the United States—to procure the chips it needs for its vehicles have reinforced the need for greater security in the supply chain.

Pandemic-driven demand has pushed the market into an unbalanced situation, with demand exceeding supply. Legacy chips have been impacted particularly hard due to the lack of investment in fab capacity.

Again, the forces of globalization and outsourcing are exposing their limits. In recent decades, IC manufacturing has become concentrated in the hands of fewer and fewer players—almost invariably outside the Western hemisphere.

Source: Bloomberg

To its credit, the U.S. administration recognizes the threat to national security and is rethinking the previous strategy of leaving international IT investment in the hands of Wall Street. Seeking to avert future crises, the Biden administration recently called a meeting with technology leaders to discuss the restoration of IC fabrication in the U.S.

“It’s not just COVID driving changes to the global technology supply chain. Climate change, weather events, and the worldwide spread of nationalism have played a part, prompting an existential shift in how we manage critical supply networks beyond the crude metrics of P&L and shareholder value.”

Crypto Miners Pose Hard (Drive) Questions

If there weren’t enough disruption already afoot, a new kid is on the block and it’s threatening to start feeding on the data center’s lunch.

It came out of the blue. The sudden rise in the farming of cryptocurrency Chia sent a jolt through the enterprise storage market. Prices for large capacity hard drives jumped 15% over night, with crypto miners buying large cap drives for their mining rigs.

For those not familiar with Chia, which I certainly was not, the currency uses a proof-of-space concept—for which hard drive and solid state storage is the optimal platform—rather than the computational approach adopted by Bitcoin and Ethereum, which draws on energy-intensive compute.

Using storage in this way promises to be more energy efficient—one of the major criticisms leveled against crypto mining—and accessible to the general population. But it’s not without its challenges.

Unlike the standard supply chain model in which customers and manufacturers communicate openly about their needs, Chia miners are an unknown entity. They consist of individuals and crypto farms without a direct connection to the manufacturers, making it near impossible to confidently accommodate them.

It is difficult to ascertain how long this phenomenon will last, what the long-term effect on supply will be, and whether the demand spike will disappear as quickly as it arrived.

Moreover, it sets up an awkward dilemma for the HDD manufacturers. As they continue to position themselves as the low-cost alternative to SSD, can they simultaneously pad the margins by meeting the needs of the crypto mining craze?

What we do know is that Chia has added pressure to an already tight HDD supply chain.

Market Fundamentals

Despite the current pressure points and uncertainty, the long-term trajectory for data center storage remains favorable.

For 2020, combined SSD and HDD shipments totaled 1.2 zettabytes, with shipped HDD capacity surpassing one zettabyte of data for the first time. The outlook for SSD manufacturers is similarly rosy. In recent analysis, IDC projected sales of PCs and notebooks—a big market for solid state storage—will grow 18% in 2021, after a 12.9% increase in 2020.

For enterprise server and storage sales, it’s true that spending was less buoyant in 2020 as CIOs reined in budgets and the cloud hoovered up pandemic-driven demand for SaaS. No surprise then that IT spend is expected to rebound in line with the economy, with hyperscale demand poised to grow 20% in Q2 alone.

In a related sign of resurgence, data center demand for high-capacity nearline hard drives is growing, with one manufacturer reporting that product is tight and customers are clamoring for drives.

Supply Chain Stressors

How bad is the IC shortage? It was bad enough that WDC sent out a note to its customers indicating that lead times have been extended due to IC challenges.

No doubt that the requests for upside will result in significantly elongated lead times and prices will increase. This will put additional pressure on SSD supply, which was already tight.

Restricted controller supplies, due to lack of foundry space, will further stress SSD manufacturing. Samsung notified clients that production of its PCIe SSDs is being disrupted by low supplies of controller chips, with production unlikely to restore until May. Further disrupting the supply chain is Samsung’s facility in Austin, Texas temporarily shutting down due to a weather event.

So what does this mean for pricing? Expect to see SSD prices increase in the 5% to 10% range over the next few months. For HDD, anticipate price hikes in the 3% to 5% range.

Spindle Wars

Another notable stressor is Seagate’s spat with Nidec, which owns 85% of the motor market (and also supplies back plates), over pricing and IP.

Moving to an alternate supplier— Minebea Mitsumi in Seagate’s case—may address the pricing issue but could throw up new problems in its wake:

What does it mean for those drives already qualified with the hyperscalers? Will they have to be requalified?

There will certainly be kinks to work through.

While Seagate has reportedly built up its nearline inventory, it’s not clear if this is to help with the supplier transition or in anticipation of an expected surge in hyperscaler demand.

SSD to eliminate HDD?

The protracted tussle between SSD and HDD shows no sign of abating.

While SSD has made significant inroads in recent years, HDD remains the dominant technology for bulk storage needs—and by most accounts will remain so throughout the 2020s .

Not so fast, says David Floyer, whose recent Wikibon article threw fire on this argument, postulating that the twin forces of SSD and tape will replace HDD by 2026.

Floyer’s hypothesis presents interesting arguments:

- He starts by stating “Wright’s law,” which equates efficiencies gained from scale manufacturing with an annual expense decline of 10%-15%.

- As SSD prices drop, the lower cost will increase demand for the product. In turn, this will allow manufacturing costs to be amortized across increasing unit volumes, eating into HDD sales.

- Conversely, shrinking HDD volumes will increase the development costs of new hard drive technologies, as there are fewer drives to amortize costs against. This, in turn, will negatively impact HDD’s cost benefit.

His hypothesis focuses on the use of low cost QLC-based SSD in conjunction with data reduction approaches used by companies like Vast Data.

Examining the Data

At face value, Floyer presents a convincing argument—but as always, the devil is in the detail.

Jumping out at me is Floyer’s citing 2020 HDD and NAND capacity shipments at 410 exabytes and 435 exabytes respectively, while both TrendFocus and Coughlin Associates list in excess of one zettabyte of shipped HDD alone for the past year. I cannot explain the source of Floyer’s data.

The next query I have is around cost per TB, where Floyer pegs HDD at $20.20 per TB for HDD and SSD at $128. True, at Horizon, we recently sold a midsize integrator 12TB drives at $224, which works out to $18.66 per TB and is somewhat close to Floyer’s figure.

That said, a hyperscaler is paying an estimated $13-$14 per TB, and it’s the cloud data centers that are the primary destination for the bulk of hard drives. Using the latter price point moves the SSD cost premium over HDD from Floyer’s 5.8x to as high as 9x.

According to this calculation, HDDs remain much more price competitive than SSD, even within his five-year timeframe.

Seagate’s CTO John Morris would seem to agree. Morris states that demand for low cost storage from the hyperscaler market is growing at a 30% rate and cost reductions for both SSD and HDD are tracking at 20% per year. In this scenario, he argues, there clearly is room for SSD and HDD to coexist based on use case.

He also questions Floyer’s approach in comparing HDD versus SSD in how Floyer accounts for data deduplication and reduction. With HDD, those two activities have already been performed before the data is written to the hard drive, Morris says.

Granted, Floyer presents a compelling argument in his wide-ranging and detailed analysis. While he may ultimately prove to be right, let’s keep in mind there is a large installed base of spinning drives out there that allows Seagate to sell on average 4-5 million mission critical (2.5” 10k RPM) drives alone per quarter.

In addition, in talking to a NAND/SSD manufacturer, it appears there still are issues to be sorted through with QLC. Although all-flash arrays offer exciting possibilities, for many it comes down to cost. Meanwhile, tape is too slow and space consuming.

Perhaps Intel’s announcement of PLC NAND (penta cell) will drive costs to the level that spells the end of the hard drive. That said, one can look to Intel’s rollout of its 10 nanometer CPU as evidence that one doesn’t always get it right the first time, or even the second.

Finally, let’s not forget that the hard drive manufacturers have been at this for a while.

Capacity Remains King

One thing everyone seems to agree on is the importance of the HDD makers driving up their capacities over time.

For hard drives, HAMR is critical to increasing areal density and maintaining HDD’s price advantage over SSD. But the technology is moving relatively slowly. Although Seagate shipped samples of its 20TB HAMR drive in November and will be shipping volume to a handful of key customers in 2021, mainstream HAMR volumes are not expected to ramp until 2023.

Elsewhere, we see a variety of incremental approaches mixed and matched to increase capacity:

- Toshiba is utilizing a thinner glass substrate to allow for a 10-platter drive in the 3.5” format. It also released an energy-assist drive in 16TB and 18TB capabilities utilizing flux control—microwave assisted magnetic recording (FC-MAMR).

- WD released its 18TB partial microwave-assisted magnetic recording technology (ePMR). It will utilize ePMR and SMR to reach 20 TB.

- All three of the manufacturers use two dimensional magnetic recording (TDMR) to increase capacity. Multi-actuator arms are deployed to double read write speeds to close the performance gap with SSD.

What happens with HAMR over the next few years is perhaps never more important to the future of hard drive technology.

A Changing World

From HDD vs SSD and reshoring to crypto mining and pricing wars, one thing is clear: the data center supply chain remains subject to extreme uncertainty for some time yet.

Pandemic notwithstanding, the great power struggle between China and the United States will continue to drive much of this volatility. While the U.S. was the world’s technology leader for decades, China has made great progress in recent times asserting its technological prowess.

In this tussle over technology, we will watch intently as two ideologies pitch battle against the other. Has the U.S. capitalist model surrendered national interest to short-terms profits? Is the Chinese planned economy with a single point of leadership a more effective approach?

Or is there a better alternative to this zero-sum game? In the face of so many global challenges that ultimately demand our cooperation, forging a third way that benefits all parties might be the next best move we can make.

*

Stephen Buckler is Horizon Technology’s chief operating officer. Connect with Stephen on LinkedIn.

For expert support with the procurement and replacement of your data center hardware, get in touch with Horizon Technology and let us know how we can help.